Let’s Seize the Opportunity – It’s time to Work Together

Ken Charbonneau, FCPA, FCA, ICD.D

Chair, Canada's Auditing and Assurance Standards Board

Recently retired from KPMG, where he was Partner, Assurance, Ken Charbonneau has more than 40 years of business experience. He has provided assurance, accounting, and advisory services to public and private organizations in the technology, media, and communications sectors, amongst others.

Recently retired from KPMG, where he was Partner, Assurance, Ken Charbonneau has more than 40 years of business experience. He has provided assurance, accounting, and advisory services to public and private organizations in the technology, media, and communications sectors, amongst others.

While with KPMG, Ken served in several leadership roles, including Business Unit Professional Practice Partner for 15 offices in eastern Canada, Partner-in-Charge at the firm’s national marketing and communications group in Toronto, and a leader of the audit practice and technology industry group in Ottawa. As a community volunteer, he has been active on boards and committees of various not-for-profit organizations throughout his career.

In 2016, Ken was awarded the Fellowship of the Institute of Chartered Accountants of Ontario (FCPA).

(Originally published on July 9, 2020 via LinkedIn Articles.)

When things go wrong, it’s easy to play the blame game. But our capital markets are too important. We need a collaborative approach to meet the public interest needs of Canadians. Let’s seize the opportunity as we emerge from the pandemic.

The Environment

The proper functioning of our capital markets depends on credible, high-quality financial, and non-financial information. This information enables investors and other stakeholders to make well-informed decisions.

Today, financial statements and continuous disclosure documents are the focus of Canadian corporate reporting. Tomorrow, corporate reporting will also include disclosure of many different forms of emerging financial and non-financial information to capture all relevant information about an organization.

Canadian corporate reporting includes information derived from financial statements, such as non-GAAP measures and other key performance indicators related to financial and operational metrics. While awareness is relatively low here, there are signs that corporate reporting in Canada is evolving to include broader information related to environmental, social, and governance (ESG) factors.

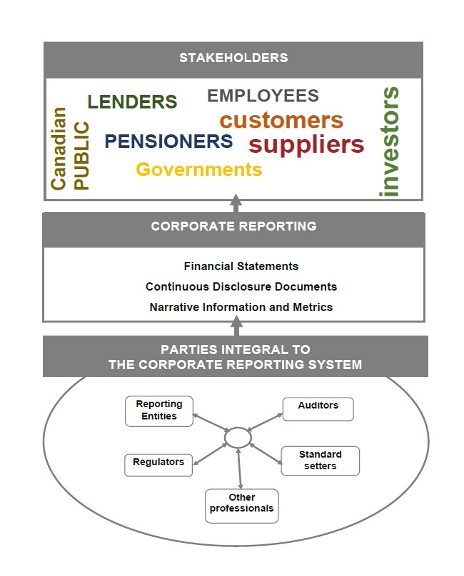

Stakeholders in our capital markets, and their needs, are rapidly expanding and changing. Stakeholders now include employees, pensioners, customers, suppliers – the Canadian public. There are growing expectations that entities need to provide more information about the wider impact they have on society and the non-financial resources they employ or impact. At the same time, Canadians are frequently using other forms of financial information in addition to financial statements to support decision making.

The Challenge

To maintain trust in companies, and confidence in corporate reporting, all parties in the corporate reporting system must contribute toward the collective goal of delivering credible, high-quality information to Canadians.

The corporate reporting system involves five parties:

1. Reporting entities – Management and Directors

2. Auditors

3. Regulators – Audit firm inspectors, Securities Regulators, and Prudential Regulator

4. Standard setters – Accounting, Auditing, and Other Information (ESG)

5. Other professionals – Chartered Professional Accountants and Legal Profession

Each party plays different but interconnected roles.

In my view, the strength of this system and the quality of Canadian corporate reporting relies on two factors:

• The rigour of all parts of this system and the quality of each of the parties; and

• the parties’ ability to work together to proactively address the expanding and changing needs of Canadians.

However, these parties generally act autonomously and sometimes collaborate informally. There is currently no framework or process for them to work together toward the public interest goal of high-quality corporate reporting. A couple of examples illustrate the need and benefits of a collaborative response to corporate reporting challenges.

The business environment is rapidly changing and becoming increasingly complex. The complexities of business and speed of change – including the rapid adoption of evolving technologies – are having a significant effect on business models and operations, and economies.

In late 2017, there was barely a handful of Canadian public companies with material cryptocurrency transactions or balances in their business operations. By the spring of 2018, the number of companies using cryptocurrencies or announced intentions to do so rose to a level that demanded the urgent attention of all the parties in the Canadian corporate reporting system. However, these parties had little or no experience with cryptocurrencies and the underlying blockchain technology as cryptocurrency was the first significant use of this technology.

It was clear that all parties needed to understand the impact of blockchain and other emerging technologies. Management and directors needed to implement sufficient internal controls, auditors needed to develop new audit methodologies and involve technology specialists in their work, audit and accounting standards were challenged to be fit for purpose, regulators needed to implement requirements that protect the capital markets and the accounting profession needed to provide guidance.

To successfully address the corporate reporting challenges of blockchain and other emerging technology businesses, timely collaboration by all parties was necessary. Although not timely, several of the parties initiated a collaborative approach to understand and address the financial reporting challenges and develop a response that reflected everyone’s input.

The importance of a collaborative approach is reinforced by COVID-19. The impact of the pandemic was swift, shutting down or significantly curtailing a large swath of the Canadian and global economy. It created an unprecedented level of uncertainty about the economy, future earnings, and many other inputs that represent fundamental elements of corporate reporting. All aspects of corporate reporting are impacted in ways the parties involved in the corporate reporting system have never seen.

COVID-19 challenged all parties in the corporate reporting system to respond and adapt quickly. Collaboration involving almost all parties, beginning with strong communication and information sharing, and leading to actions has so far been effective in addressing many of the corporate reporting challenges. But it could have been timelier, more coordinated, efficient, and effective.

In contrast to a collaborative approach, I think it is important to highlight that, over the past few years, several other countries chose to focus mainly on the audit and auditors to address concerns with financial reporting.

Perhaps the most prominent example is the United Kingdom where the immediate response to company failures was criticism of the audit profession and the launch of three government reviews: Two focused on auditing and the audit profession and the third focused on the regulator – including its role and power to regulate the audit profession.

While changes to the audit profession may be required to improve audit quality, I question whether this can resolve all corporate reporting challenges. I believe all five parties involved in the corporate reporting system must deliver quality and work together to maintain confidence in corporate reporting.

To use a truly Canadian example, it takes more than the last line of defense – the goalie – to win a hockey game. The other players, coaches, staff, management, owners, referees, and league must work together to collectively deliver a positive outcome.

Because of the interconnected roles, a collaborative response involving all parties is necessary to maintain the delivery of credible, high-quality corporate reporting.

The Solution

I see an opportunity to enhance and maintain trust in corporate reporting in Canada by embedding collaboration in the corporate reporting process.

It’s time that the five individual parties establish a collaborative framework for the delivery of credible, high-quality information that maintains the trust of Canadians. The key benefits of this approach are solutions that reflect the collective response of the parties in the corporate reporting system. Recent experience with cryptocurrency and COVID-19 demonstrates that much can be achieved when parties in the corporate reporting system collaborate to understand challenges and develop solutions. It should never be expected that one party can solve corporate reporting issues and challenges.

It’s time for all parties to work together. For example, Canadians are questioning whether the corporate reporting system ensures adequate information is disclosed when an entity does not have the resources it needs to continue operating – often referred to as going concern information. Because of the interconnected roles, this question requires a proactive and collaborative response of all parties:

• Entity management must complete a going concern assessment and disclose significant concerns, and directors need to provide robust oversight of management and the auditor, all in accordance with accounting standards and regulatory requirements.

• Auditors must perform appropriate procedures on management’s going concern assessment and provide an audit opinion in accordance with audit standards.

• Audit firm inspectors must assess the performance of auditors and other regulators need to establish rules for the parties that protect investors.

• Accounting standards need to include requirements that promote robust going concern assessments and adequate disclosures, and audit standards need to include requirements that promote a thorough examination of management’s assessment and disclosures with the results communicated in an informative auditor’s report.

• Effective guidance from the accounting and legal professions is necessary for management, directors, and auditors to effectively perform their responsibilities.

If the corporate reporting system and all parties integral to that system do not deliver credible, high-quality information about an entity’s ability to continue as a going concern, there is risk of significant financial loss and related problems – and an erosion of trust by Canadians. In addition, we risk triggering a crisis that generates a less than optimal response like that experienced in other countries. We do not want to experience the grip of emotion and crisis, followed by a political response that may not generate a quality solution that addresses the real issues.

Going concern is only one of several corporate reporting challenges that need to be addressed. They include fraud, non-GAAP information, regulatory reform, environmental, social and governance reporting, and the evolving impact of COVID-19.

Government regulation and intervention is proportional. The Canadian corporate reporting model is relatively free of government oversight, which is unique compared to many other countries. This model has served Canadians well and will only continue if those involved collaborate to proactively address current and future corporate reporting challenges.

Where we go from here depends on the willingness of representatives of the five parties in the corporate reporting system to engage in meaningful discussion and the courage to establish a framework that embeds collaboration in the Canadian corporate reporting system.